Are You 65 Years Or Older Or Disabled? Here Is What You Should Know About The Property Tax Deferral.2/4/2022

0 Comments

Big news! During the past 40 years, there was no consequence if the appraisal district or the appraisal review board ignored the laws regarding property tax hearings including the following:

Huge Change -If the TLO is notified of unlawful behavior by the appraisal review board, the TLO is required to investigate. If the complaint is valid, the appraisal district board of directors is required to address the issue with the chairman of the appraisal review board. This is a Huge Change since the appraisal district board of directors has routinely dismissed complaints about unlawful behavior by the appraisal review board since they are “separate and apart” from the appraisal district. New Statute – A person who owns property in an appraisal district or the chief appraiser of an appraisal district may file a complaint with the taxpayer liaison officer for the appraisal district alleging that the appraisal review board established for the appraisal district has adopted or is implementing hearing procedures that are not in compliance with the model hearing procedures prepared by the comptroller under Section 5.103 or is not complying with procedural requirements under this chapter. The taxpayer liaison officer shall investigate the complaint and report the findings of the investigation to the board of directors of the appraisal district. The board of directors shall direct the chairman of the appraisal review board to take remedial action if, after reviewing the taxpayer liaison officer’s report, the board of directors determines that the allegations contained in the complaint are true. The board of directors may remove the member of the appraisal review board serving as chairman of the appraisal review board from that member’s position as chairman if the board determines that the chairman has failed to take the actions necessary to bring the appraisal review board into compliance with Section 5.103(d) or this chapter, as applicable. New Statute Providing for Option for Binding Arbitration if Appraisal District or Appraisal Review Board Do not Comply with Lawful Hearing Procedures SECTION 20. Chapter 41A, Tax Code, is amended by adding Section 41A.015 to read as follows: Sec. 41A.015. LIMITED BINDING ARBITRATION TO COMPEL COMPLIANCE WITH CERTAIN PROCEDURAL REQUIREMENTS RELATED TO PROTESTS. (a) A property owner who has filed a notice of protest under Chapter 41 may file a request for limited binding arbitration under this section to compel the appraisal review board or chief appraiser, as appropriate, to: (1) rescind procedural rules adopted by the appraisal review board that are not in compliance with the model hearing procedures prepared by the comptroller under Section 5.103; (2) schedule a hearing on a protest as required by Section 41.45; (3) deliver information to the property owner in the manner required by Section 41.461; (4) allow the property owner to offer evidence, examine or cross-examine witnesses or other parties, and present arguments as required by Section 41.66(b); (5) set a hearing for a time and date certain and postpone a hearing that does not begin within two hours of the scheduled time as required by Section 41.66(i); (6) schedule hearings on protests concerning multiple properties identified in the same notice of protest on the same day at the request of the property owner or the property owner’s designated agent as required by Section 41.66(j); or (7) refrain from using or offering as evidence information requested by the property owner under Section 41.461 that was not delivered to the property owner at least 14 days before the hearing as required by Section 41.67(d). (b) A property owner may not file a request for limited binding arbitration under this section unless: (1) the property owner has delivered written notice to the chairman of the appraisal review board, the chief appraiser, and the taxpayer liaison officer for the applicable appraisal district by certified mail, return receipt requested, of the procedural requirement with which the property owner alleges the appraisal review board or chief appraiser failed to comply on or before the fifth business day after the date the appraisal review board or chief appraiser was required to comply with the requirement; and (2) the chairman of the appraisal review board or chief appraiser, as applicable, fails to deliver to the property owner on or before the 10th day after the date the notice is delivered a written statement confirming that the appraisal review board or chief appraiser, as applicable, will comply with the requirement or cure a failure to comply with the requirement. (c) Except as otherwise provided by this subtitle, the failure to comply with a procedural requirement listed under Subsection (a) is not a ground for postponement of a hearing on a protest. An appraisal review board may cure an alleged failure to comply with a procedural requirement that occurred during a hearing by rescinding the order determining the protest for which the hearing was held and scheduling a new hearing on the protest. (d) A property owner must request limited binding arbitration under this section by filing a request with the comptroller. The property owner may not file the request earlier than the 11th day or later than the 30th day after the date the property owner delivers the notice required by Subsection (b)(1) to the chairman of the appraisal review board, the chief appraiser, and the taxpayer liaison officer for the applicable appraisal district. (e) A request for limited binding arbitration under this section must be in a form prescribed by the comptroller and be accompanied by an arbitration deposit payable to the comptroller in the amount of: (1) $450, if the property that is the subject of the protest to which the arbitration relates qualifies as the property owner’s residence homestead under Section 11.13 and the appraised or market value, as applicable, of the property is $500,000 or less, as determined by the appraisal district for the most recent tax year; or (2) $550, for property other than property described by Subdivision (1). (f) The comptroller shall prescribe the form to be used for submitting a request for limited binding arbitration under this section. The form must require the property owner to provide: (1) a statement that the property owner has provided the written notice required by Subsection (b); (2) a statement that the property owner has made the arbitration deposit required by this section; (3) a brief statement identifying the procedural requirement with which the property owner alleges the appraisal review board or chief appraiser, as applicable, has failed to comply; (4) a description of the action taken or not taken by the appraisal review board or chief appraiser regarding the procedural requirement identified under Subdivision (3); (5) a description of the property to which the award will apply; and (6) any other information reasonably necessary for the comptroller to appoint an arbitrator. (g) On receipt of the request and deposit under this section, the comptroller shall appoint an arbitrator from the registry maintained under Section 41A.06 who is eligible to serve as an arbitrator under Subsection (p) of this section. Section 41A.07(h) does not apply to the appointment of an arbitrator under this section. Blog AuthorPatrick O’Connor, MAI, Owner and President Patrick O’Connor has been active in reducing property taxes, providing expert witness testimony and appraising commercial real estate property since 1983. Pat is active in publishing analyses and data with respect to the real estate market, while being a highly regarded media spokesperson for the real estate community. He holds a MAI, the highest achievable designation from the Appraisal Institute, and is a licensed senior property tax consultant. Pat earned a Master of Business Administration from Harvard University. In 2001, he authored the first definitive consumer guide to Texas property taxes, Cut Your Texas Property Taxes. Property Tax Protection Program™ Enroll Now Learn MoreNo cost to enroll RecentsProperty Tax Reduction ConsultantsProperty Tax ReductionDo property taxes increase if assessed value does?This tax bill CAN’T be right!?When should a tenant be removed from the rent roll?Are the appraisal district commercial property values for 2021 reasonable?Do commercial property owners win their appeals?Questions about your homestead exemption?Why was my commercial property tax assessment raised during COVID?What magnificent gifts did the 2021 Texas Legislature provide property owners?Property owners seeking to enroll in the Property Tax Protection Program™

Property Tax Protection Program™ ENROLL NOW! Many companies during the pandemic have not been involved in buying equipment in the past year and have stepped into conserving cash. The upside is that the chances for companies to claim the same depreciation tax deductions as they have been during the previous years are very few. However, a cost segregation study can help you accelerate depreciation deductions which in turn result in reducing your taxes and increasing your cash flow. With the enhancements of depreciation-related tax breaks by the Tax Cuts and Jobs Act (TCJA), CSS benefits have increased when compared to the previous years.

Instead of following the same old method of calculating the depreciation of an asset by dividing its value by 27.5 years, a cost segregation study divides a property into different components and helps the owner depreciate an asset over a shorter period of time. This in turn results in reducing the taxable income and increases the cash flow. The different components here include personal property, land improvements, the structure of a building, and land assets. Building componentsExampleDepreciation period Personal propertyFurniture, equipment, phone lines, signage, carpeting, etc.5 to 7 years Land improvementsParking lots, sidewalks, fences, etcOver 15 years Structure of a buildingRoof and the foundation of a buildingOver 27.5 years. Land assetsNilNot depreciatedCALCULATING THE TAX SAVINGSA cost segregation study when conducted at the right time can yield a lot of benefits. A CSS exactly identifies which building component can be treated as a personal property that can be depreciated over a period of 5 or 7 years or as land improvements that can be depreciated over a period of 15 years. By allocating the costs accordingly, you can accelerate the depreciation deductions and reduce your property tax bill. Do not forget bonus depreciation. If the assets qualify, the tax savings can be great. CONDUCTING A COST SEGREGATION STUDYAs per the IRS audit technique guide, there is no qualification described as such for a cost segregation preparer. CSS conducted by civil engineers is considered good when compared to the CSS conducted by people who do not have a civil background. Apart from this, experience and expertise in the field of cost segregation matter a lot. TAX BENEFITS THAT ARE REWARDINGCost segregation study is a valuable investment even though it depends on certain facts and circumstances. Though it might cost you a reasonable amount, the tax benefits from it are long-term and worthwhile. CSS is a good idea to reduce your property taxes as:

Texas property tax rates have always been skyrocketing and many property owners out there are expecting to see a tax break because of the current economic situation, but sadly it is not on the horizon. With COVID-19 hitting the real estate market, Texans are not likely to see any tax break in 2020. The opportunity to freeze taxes is slim as well. Property owners are left with just one choice, and it is none other than protesting property taxes.

WHY NO TAX BREAKS IN 2020?There are two major reasons.

FILING A PROPERTY TAX APPEALFiling an appeal is the best way to reduce the tax burden and is also your responsibility as a property owner. Pay only your share of the property taxes, not anymore. By appealing your property taxes, you can reduce a significant amount of taxes you owe. Doing this every year helps you save hundreds and thousands of dollars. You can protest your own property taxes for free, or hire a company to do it for you. If you wish to protest on your own, the most important thing you can do is get the HB201 evidence package from the appraisal district. It will include all the details the county appraisal district included in order to come up with their evaluation. Another important note is to ALWAYS bring photos with you to the hearings. The process of protesting can be tedious, it starts off with filing a form with the county appraisal district, you then meet with the CAD and try to resolve the issue. If an agreement is not reached you will have to file a written notice of protest with the ARB. If you don’t agree you can then appeal to the district’s court else opt for binding arbitration or file with the SOAH. If you protest on your own and having a hard time, professional companies, like O’Connor, can do it for you. ENROLL TODAY IN THE PROPERTY TAX PROTECTION PROGRAMYour property taxes will be aggressively appealed every year by the #1 property tax firm in the country. If your taxes are not reduced you PAY NOTHING, and a portion of the tax savings is the only fee you pay when your taxes are reduced! Many FREE benefits come with enrollment. Know more @ https://www.cutmytaxes.com/protesting-property-taxes-during-a-pandemic/  Most homeowners have the question, “Do I get a tax break on the money I’ve spent?” on their minds when they are fixing up their homes. The answer differs based on the kind of improvements and how well the expenses incurred are tracked. In most cases, the money that is spent on the capital improvements such as adding an additional bathroom or a garage, or a satellite dish helps lower the property tax bill when selling a house. The money that is spent on home improvements can be categorized into two areas, the cost of improvements and the cost of repairs.

The cost of improvements not only includes big items but also includes energy-saving home improvements. These improvements give you tax credits. The cost of repairs is not added to the basic cost. As per the IRS from the year 2018 to 2021 individuals can claim credits for the below:

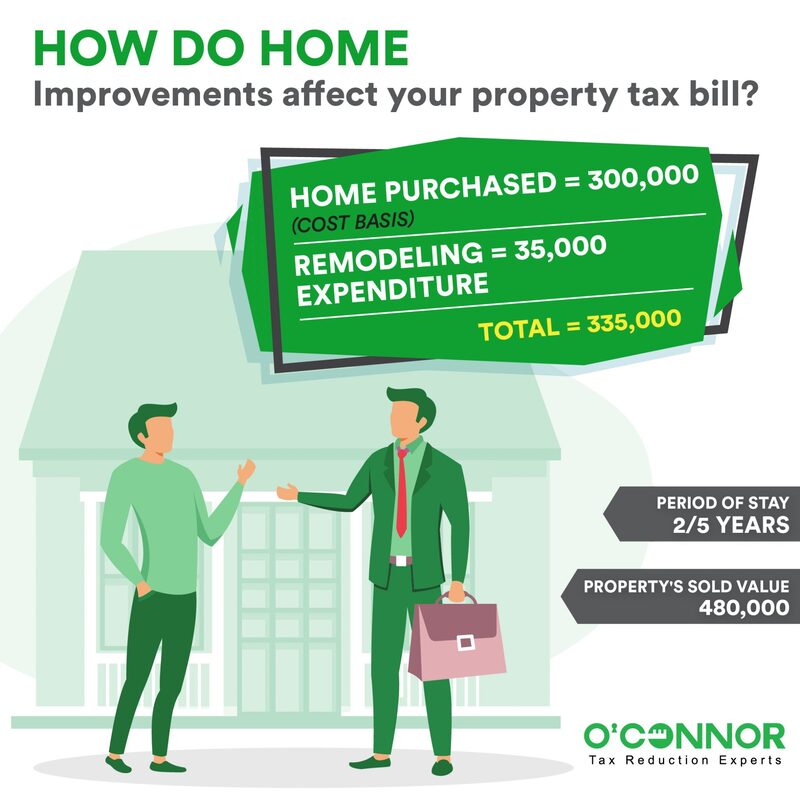

Taxable home improvements Not all the improvements you do for your house are considered home improvement. The IRS looks at it differently. According to the IRS, the capital improvements made to a property must last for more than a year and must add value to your residential property and increase its life. Capital improvements can include constructing a new bathroom. Refer to the IRS Publication 523 to check out what items qualify. However, there are limitations. The improvements made should be evident during the sale. Let us say you had made improvements to your home 7 years back by installing wall-to-wall carpeting. 5 years later you change it to a hardwood floor. At present, the wall-to-wall carpeting cannot be considered as a capital improvement. According to the IRS, repairs refer to those things that are done to maintain the good condition of a house and do not add value to the property or increase its life. How do home improvements affect your property tax bill? To know how home improvements affect your tax bill, it is important to know your cost basis. The cost basis is simply the amount of money you spend to build your house including costs such as your lawyer fee, survey charge, home inspection, etc. then add all the money spent for your property’s capital improvements. Let’s understand it better with an example: Say if you are single, you get an exemption on the profit of 180,000. If you had not considered the money you spent on remodeling, then your tax bill would have included 35,000 as well. Hence, keeping the receipts and adjusting the cost basis help you save! |

AuthorHi everybody, Archives

June 2022

Categories

All

|

RSS Feed

RSS Feed